Why You Should Always Shop Around for a Personal Loan

Comparing personal loan offers is one of the simplest ways to reduce the cost of borrowing. This article covers how lenders differ, how to check rates safely and how to choose a loan with confidence

Whether you've received a "pre-approved" offer in the mail, seen a lender's commercial on TV, or borrowed from the same company before, it's tempting to take the first loan that looks reasonable and move on.

That can be an expensive mistake.

Most people understand the importance of shopping around when making a major purchase. We compare prices when buying a car, choosing an insurance policy, or hiring a contractor. We know that spending a little time evaluating alternatives can save a significant amount of money.

A personal loan should be no different.

Although it may not feel like you're buying something, you are. A loan is simply a financial product and the price of that product is the interest and fees you pay over time. Just as you wouldn't want to overpay for a car or a new appliance, you should avoid overpaying for money.

The good news is that comparing lenders has never been easier. Most lenders allow you to check your rate online without affecting your credit score and comparison websites can help you review dozens of offers in minutes—all of which could save you hundreds or even thousands of dollars over the life of a loan.

The Same Borrower Can Receive Very Different Offers

The biggest reason to shop around is simple: lenders don't all see you the same way.

As we've discussed in this article, you don't have a single credit score. Different lenders use different scoring models, underwriting systems and lending criteria. One lender might place significant weight on your income, another might focus on your payment history, while a third might care more about your existing debt levels.

As a result, the exact same borrower can receive dramatically different offers from different lenders.

You might appear to be a high-risk borrower to one lender and an excellent customer to another. Because lenders price loans according to the risk they believe they're taking, those differences can have a major impact on the interest rate and fees you're offered.

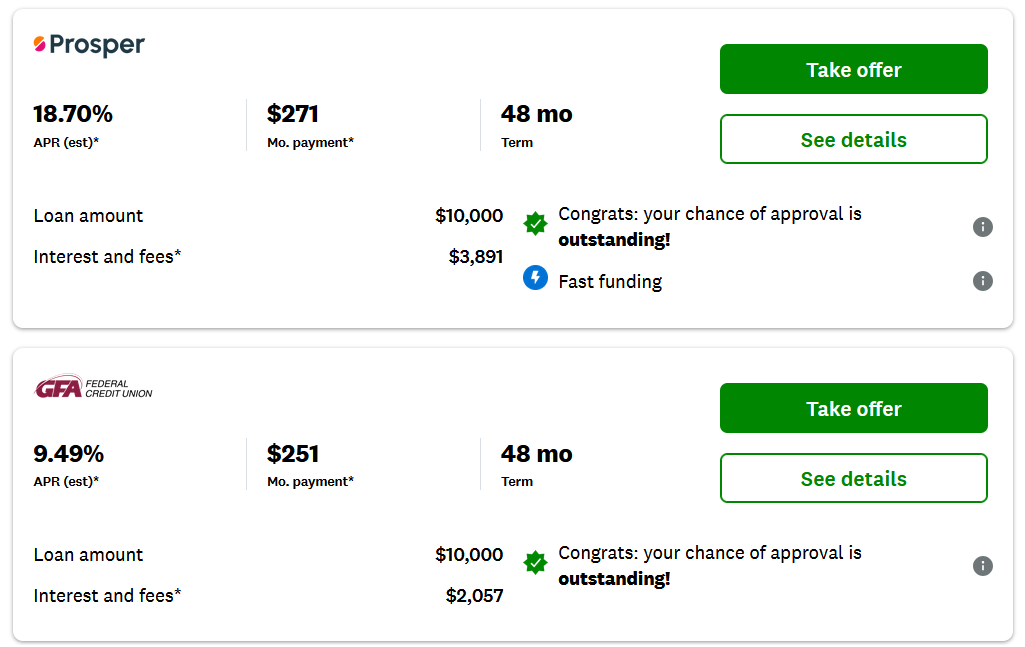

The screenshot above comes from Credit Karma, where I was comparing personal loan offers. Both lenders were offering a $10,000 loan with a four-year repayment term. At first glance, the offers look fairly similar. But the details tell a very different story. The Prosper loan carries an APR of 18.7%, while the GFA Federal Credit Union loan comes in at 9.49%.

That difference translates into approximately $1,834 in additional interest and fees over the life of the loan.

Had I accepted the first offer without looking elsewhere, that money would have gone straight to the lender with no real upside to me.

Checking Your Rate Usually Won’t Hurt Your Credit Score

One reason people avoid shopping around is fear of damaging their credit score. Fortunately, that concern is often misplaced.

Most lenders now offer prequalification tools that use a soft credit inquiry rather than a hard inquiry. Soft inquiries do not affect your credit score, allowing you to compare offers from multiple lenders without any negative impact on your credit.

It's important to understand that prequalification offers are not guaranteed approvals. Before funding a loan, most lenders will perform a hard credit inquiry and verify information such as your income and employment. The final offer may differ from the prequalified offer.

Still, modern loan shopping is far more credit-friendly than many borrowers realize. In many cases, you can compare multiple offers with little to no downside. That's a major advantage for consumers and it's one you should take full advantage of.

Your Loyalty Could Cost You

Many people naturally start their search with a lender they've used before. That makes sense. Familiar companies feel safer and a positive past experience can create trust.

Getting a loan is ultimately a business transaction. Lenders don't approve loans because they want to help you. They approve loans because they believe they can make money while managing their risk.

If you've had a good experience with a lender in the past, they should absolutely be part of your comparison process. In some cases, your repayment history with them may help you qualify for a competitive offer.

But there's no guarantee that they'll provide the best rate, lowest fees or most favorable repayment terms available to you. If two grocery stores sold the same products, but one consistently charged 20% more than the other, you probably wouldn't keep shopping there out of loyalty alone. The same principle applies to borrowing.

A lender doesn't need to be your favorite lender. It just needs to offer the best deal for your situation.

Online Comparison Tools Can Help

Fortunately, comparing lenders has never been easier.

You can visit individual lender websites and check your rate directly, but there are also comparison platforms such as Credit Karma, NerdWallet and Credible that allow you to review offers from multiple lenders in one place.

Depending on the platform, you may be able to compare dozens—or even hundreds—of potential offers within minutes.

Tip

If you're using a comparison website, try to choose one with a large network of lenders. The more lenders included, the less likely you are to miss a better offer elsewhere. Also remember that many comparison sites earn money through commissions. Featured recommendations aren't always based solely on what's best for you, so it's worth doing a little independent research before making a final decision.

Once you've identified an offer you're interested in, you'll typically complete the application directly on the lender's website. This is often the stage where a hard credit inquiry occurs.

Some comparison sites even offer "best rate" guarantees. If you find a better rate elsewhere, they may provide a cash bonus or other compensation. While these guarantees can be useful, it's always worth reading the terms and conditions carefully.

Don't Be Rushed

Shopping around is also about adopting the right mindset.

Many lenders market aggressively using phrases like:

- "You’re pre-approved"

- "Limited-time offer"

- "Exclusive rate"

- "Act now"

These messages are designed to create urgency. The goal is simple: get you to make a decision before you've had time to explore alternatives.

A pre-approved offer may be worth considering, but it doesn't mean it's the best loan available to you. In many cases, it's simply an advertisement designed to encourage you to apply.

The more rushed you feel, the more careful you should be. Shopping around helps protect you from making emotional decisions. Instead of acting on impulse, you gain a better understanding of the market and the options available to you.

When you know what alternatives exist, you're far more likely to choose the loan that actually fits your needs.

Shopping Around Is About Empowerment

At its core, shopping around is about putting borrowers back in control.

Too many parts of the financial system are designed to favor institutions that have more information, more experience and more bargaining power than consumers. Loan marketing often relies on confusion, complexity and speed. But borrowers are not powerless.

Taking the time to compare offers changes the dynamic. Instead of evaluating a single loan in isolation, you can compare competing offers and determine which lender is willing to provide the most favorable terms.

It can also be helpful to remember that lenders are competing for your business. You're looking for a loan, but lenders are also looking for customers. Viewing the process this way can encourage you to compare options more carefully and avoid feeling pressured to accept the first offer that comes your way.

After all, one of the main benefits of shopping around is having the ability to choose.

Final Thoughts

Shopping around is one of the smartest things you can do when looking for a personal loan.

Different lenders can offer dramatically different rates, fees and repayment terms to the exact same borrower. A little research today could save you hundreds or even thousands of dollars over the life of a loan.

When shopping for a personal loan, remember what you're actually doing. You're buying money. The interest rate and fees are the price. And just like any other purchase, comparing options before you buy is one of the simplest ways to avoid overpaying.

The challenge, of course, is that comparing offers can sometimes feel overwhelming. Once you've gathered several quotes, it can be difficult to determine which loan actually represents the best deal. That's why we created this guide, which explains how to compare personal loan offers and avoid common mistakes.

And since you're already shopping around, our loans page includes detailed, independent reviews of most major personal loan providers. We break down important details such as rates, fees, repayment terms and eligibility requirements to help you find the loan that's right for your circumstances.