How Credit Score Apps Make Money and What It Costs You

Credit score apps can be genuinely useful, but their business models are often built around encouraging more engagement with credit rather than true financial progress.

There are now countless apps that let you check your credit score, monitor your credit file and apply for financial products. The biggest names include Credit Karma, NerdWallet and Credit Sesame. You've probably seen their commercials on TV, waited impatiently to skip one of their YouTube ads, or noticed their logos printed across sports arenas and NBA jerseys (it was Houston).

They present themselves as tools that help people make smarter financial decisions. In many ways, they do. Millions of people have used these services to build credit, easily compare products and better understand how the financial system works.

But there's another side to this industry that receives far less attention: the business model. Credit scores can affect everything from renting an apartment to qualifying for a mortgage, but they are still only one small part of a person's overall financial health. Over time, many of these apps have blurred the line between improving your credit score and improving your actual financial situation—and that distinction is incredibly profitable.

Most credit score apps make money when users apply for financial products through their platforms. Credit cards, personal loans and balance transfers are presented as financial recommendations, but they also happen to be the products these platforms make money from.

Sometimes those recommendations are genuinely useful. A balance transfer card can help someone reduce interest payments. A secured card can help build credit history from scratch. But in other cases, people can end up opening accounts they do not really need or taking on additional debt in pursuit of a slightly better credit score.

The Business Model Behind "Free"

Services like Credit Karma and NerdWallet are free to use, but they are not free to operate.

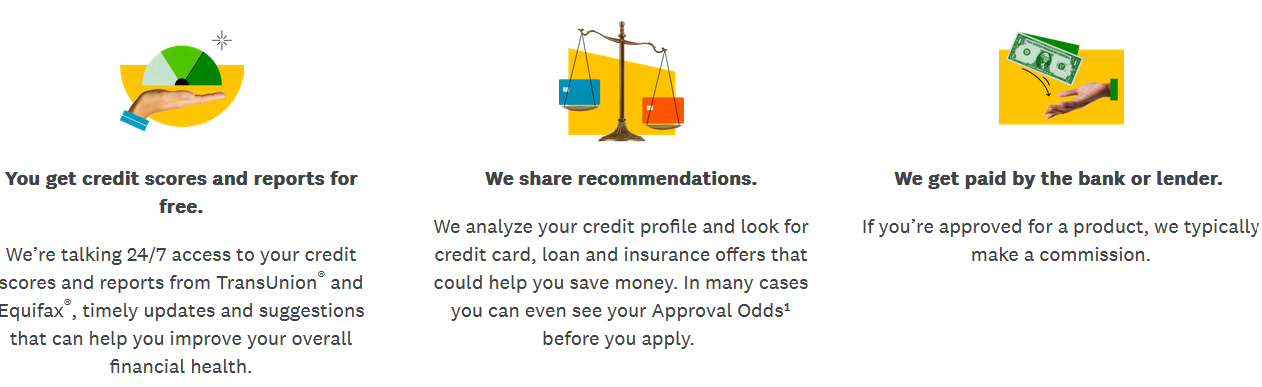

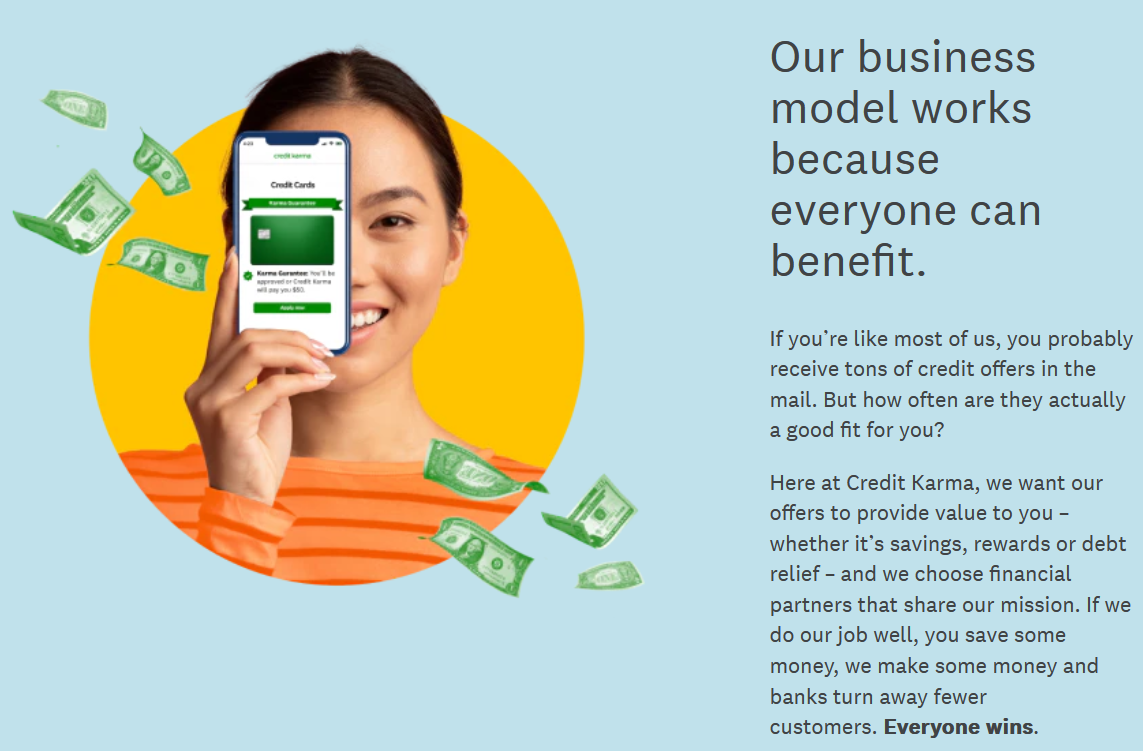

Every time you check your credit profile, those companies incur real costs. They pay credit bureaus and data providers for access to your information. They invest heavily in marketing, engineering and customer acquisition. In return, they earn commissions from banks and lenders when users are approved for financial products through their platforms—this arrangement is known as lead generation. Credit Karma actually mention this on their website (see image below), as do NerdWallet

At a basic level, this is perfectly reasonable. They built useful products that are valuable to millions of people and need a way to monetize them. It must be very expensive for NerdWallet to maintain a team of expert writers and pay whichever marketing agency came up with this admittedly catchy commercial.

The problem is not that these companies make money. The problem is that their incentives are closely tied to getting users to continually engage with credit products.

That creates a subtle but important conflict.

The more often users apply for new credit cards, personal loans or refinancing offers, the more revenue these platforms generate. Users who are financially stable, debt-free and uninterested in borrowing are far less valuable to the system.

As a result, many of these platforms are optimized not just around financial education, but around financial engagement.

The Gamification of Credit

Credit scores matter. They can affect your ability to rent an apartment, qualify for loans and access lower interest rates. But over the last decade, credit scores have also become something else: a consumer engagement hook.

While credit scores are a key component of your overall financial health, their importance has often been overstated. Most people do not need to check their credit score every week. Small fluctuations are usually meaningless, especially if you are not actively applying for credit. A temporary increase in credit card spend might lower your score slightly one month before bouncing back the next.

Yet millions of people now monitor their scores obsessively.

Why?

Because these apps transformed credit scores into something interactive and aspirational. They turned financial health into a constantly updating number that can be optimized, tracked and improved.

In isolation, that may seem harmless. But once users become emotionally invested in improving their score, they become much more receptive to product recommendations framed as "financial progress".

Open another credit card. Increase your total credit limit. Take out a balance transfer. Refinance your debt.

Sometimes these are genuinely good recommendations. Sometimes they are not. These apps often blur the line between improving your credit profile and improving your actual financial life.

The issue is that the platform recommending the product often benefits financially either way.

My Experience: From Ireland to the US

I'm from Ireland and moved to the US in 2018, when I was in my early thirties. Credit files and credit scores are not very common in Ireland. In fact, the only way to view your file there is to make an application to the Central Bank of Ireland. Moving to the US was a shock to me. I had difficulties renting an apartment, as I didn't have a credit score. I was rejected for multiple credit cards for similar reasons. But I managed to build some credit history by using some savings to get a Secured Discover credit card.

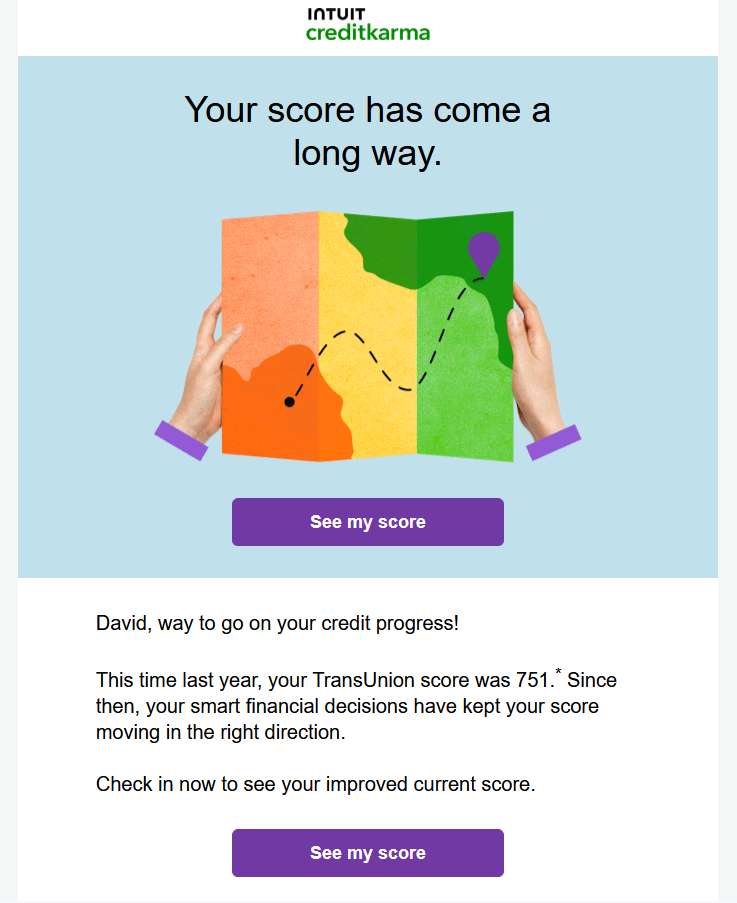

At the beginning of that journey, tools like Credit Karma and NerdWallet were genuinely useful to me. I needed to understand how the American credit system worked and how to build a financial track record from scratch. I realised that my chances of getting a good credit card with fancy perks would be limited until I could improve my score. Over the following years, with the help of these apps, I opened additional cards to take advantage of rewards programs and signup offers. Today, my score sits comfortably in the high 700s.

For people like me, once your credit reaches a certain level, there are diminishing practical benefits to constantly optimizing it. The difference between a 770 and an 810 credit score is usually far less important than these apps make it feel.

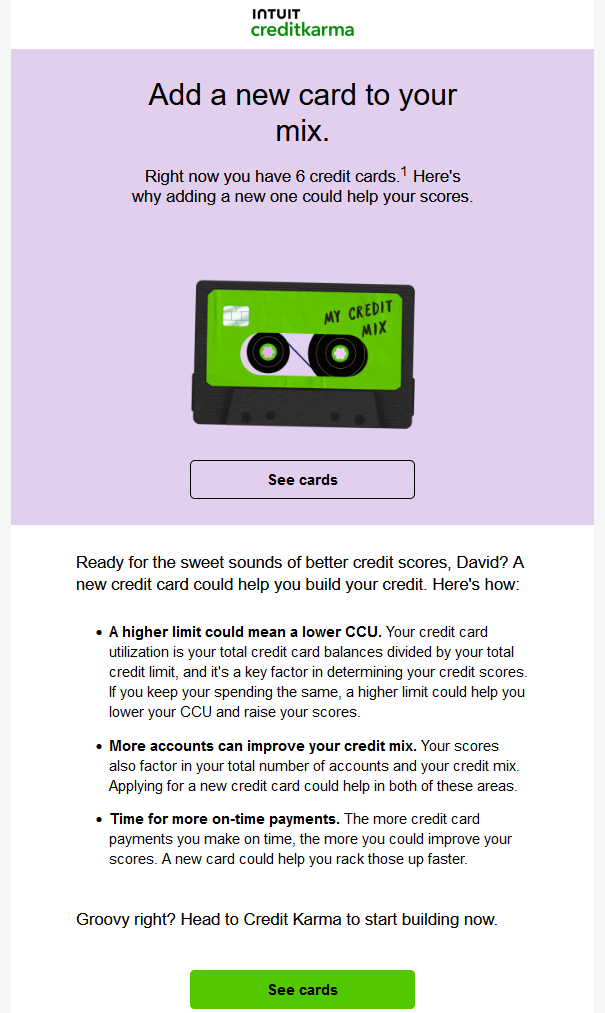

Yet the recommendations never stop.

The central message of the email is that it should be an important objective for me to improve my credit score (already in the high 700s). They provide 3 reasons as to why a new credit card (when I already have 6!) is a good way to achieve it. In reality, opening another card would likely have little meaningful impact on my financial life. With the exception of people with very limited credit history (e.g. recent immigrants from Ireland), taking out a credit card to simply improve your credit score is likely not a sensible decision.

That doesn't necessarily make the recommendation malicious. But it does reveal how the incentives work.

The platform benefits when users continue engaging with credit products, even after they may no longer need them. Someone like me still costs the platform money whenever it pulls my credit information, but generates very little revenue if I stop opening new accounts.

The Engagement Problem

This is the core problem with much of modern fintech.

Many companies claim to optimize for financial wellness, but their business models often reward something slightly different: financial engagement. Those are not always the same thing. A financially healthy customer may:

- carry little debt,

- rarely apply for credit,

- avoid unnecessary borrowing,

- and spend less time thinking about their credit score.

From a business perspective, that customer is often less profitable than someone constantly refinancing debt, opening new accounts or searching for alternative financial products.

Again, this does not mean these companies want people to fail financially. It just means that the incentives of the platform and the real long-term interests of the user are not always aligned.

What We Believe Instead

At Unbreak Finance, we think personal finance tools should reduce financial anxiety, not monetize it.

People should understand how credit works. They should have access to transparent financial products and useful educational tools. But they should not be nudged into treating debt consumption as a form of progress.

A credit score is a tool, not a lifestyle.

The financial industry has spent years encouraging people to obsess over credit while offering more and more products designed to "improve" it. In many cases, the healthiest financial decision is not opening another account. It is reducing debt, simplifying finances and disengaging from the cycle entirely.

That’s the future we want to help build.